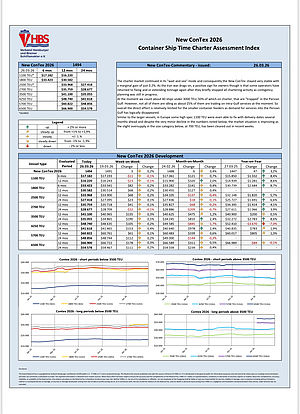

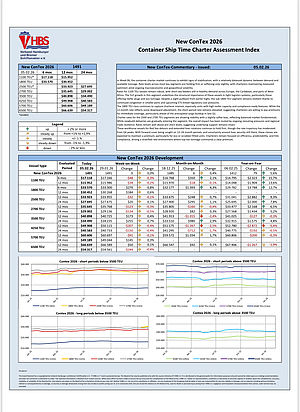

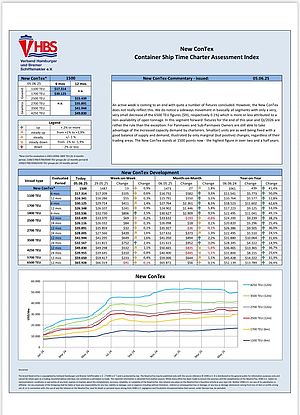

New ConTex - Alle Raten/Angaben in US-Dollar($)

|

|

New Contex | Additional Information | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 6 months | 12 months | 24 months | 12 months | ||||||||||||||

| Datum | Type 1100 | Type 1800 | Type 2500 | Type 2700 | Type 3500 | Type 4250 | ConTex | Type 2500 | Type 2700 | Type 3500 | Type 4250 | Type 5700 | Type 6500 | Type 1100 | Type 1800 | Type 5700 | Type 6500 |

| 02.07.2026 | 17.911 | 34.743 | 34.914 | 36.923 | 43.158 | 55.995 | 1572 | 27.959 | 29.482 | 36.395 | 43.700 | 50.461 | 56.450 | 16.991 | 32.205 | 64.297 | 70.350 |

| 30.06.2026 | 17.922 | 34.543 | 34.836 | 36.860 | 43.095 | 55.875 | 1568 | 27.922 | 29.382 | 36.285 | 43.670 | 50.389 | 56.472 | 17.002 | 32.007 | 64.056 | 70.267 |

Disclaimer lesen